(English below)

法人成り(個人事業主が会社を設立すること)にはさまざまな節税メリットがあり、その中の一つに給与所得控除と法人の経費の二重取りをできるというものがあります。

これは事業を行ううえで必要な経費(役員報酬も含みます)を法人で計上した上で、個人としては受け取った役員報酬から給与所得控除も差し引くことで、トータルで所得を圧縮することができる合法的な節税方法です。

今回は、その点について説明したいと思います。

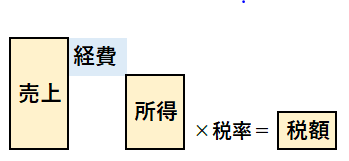

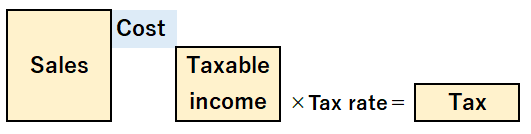

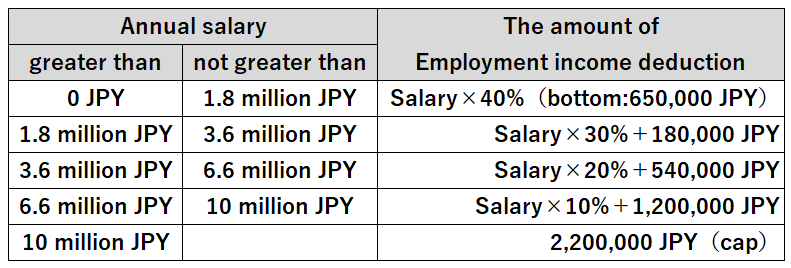

まず、個人事業主の税金の算出方法を簡単に紹介します。

【所得(売上ー経費)×税率】

ごく単純化して説明すると、1年間の売上から事業にかかった経費を差し引いて所得を算出し、その所得に税率をかけることで税額が求められます。

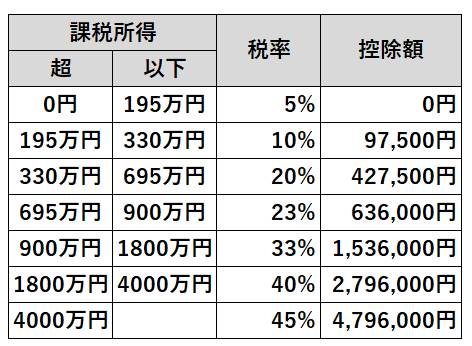

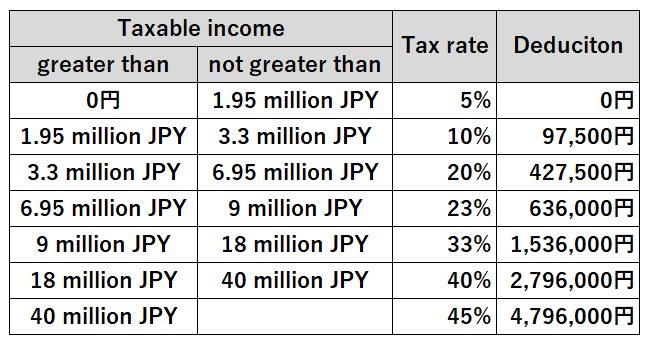

ちなみにこの税率は「超過累進税率」といい、所得が多くなるほど税率も高くなるしくみとなっています。所得が4,000万円を超えると、最高税率の45%で課税されます。

目次-Contents-

給与所得控除とは?

法人成りの節税効果を考えるうえで重要なのが給与所得控除です。

この給与所得は役員やサラリーマンとして給料をもらう方に関係するものです。給料に関する所得税を計算する際に、受け取った給料から一定額の必要経費を引くことが認められており、これが「給与所得控除」と呼ばれるものです。

これは、スーツや文具、書籍など業務に必要であるにもかかわらず、会社から支給されず自己負担しているものも少なからずあることを考慮し、サラリーマンが自己負担している経費を税金計算するうえで差し引きましょうという趣旨で存在する制度です。

前述の通り、個人事業主は実際にかかった経費を差し引ける一方、会社役員やサラリーマンの方は概算で計上した給与所得控除が適用されます。

…給与所得控除も必要経費もどちらも使えれば税金が安くなるのに、と思いますよね?

実は、この給与所得控除と必要経費の二重取りを合法的に実現することを可能とするのが法人設立なのです。

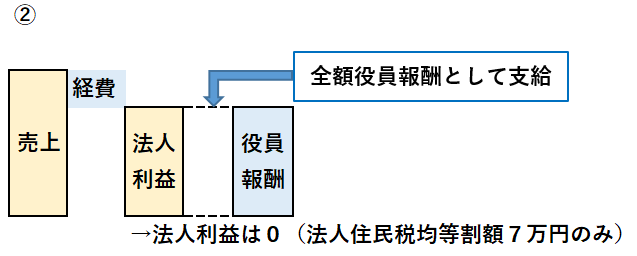

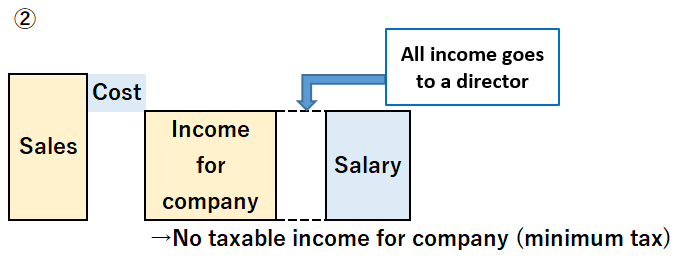

シンプルに考えるため、法人の利益と役員給与を同額に設定し、売上から経費を差し引いたの残額の利益の全部を社長(事業主)に支給したとしましょう。

法人の所得と個人の利益(所得)の算式は次のようになります。

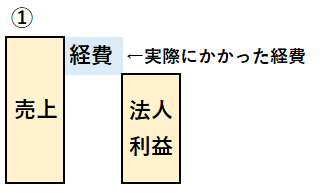

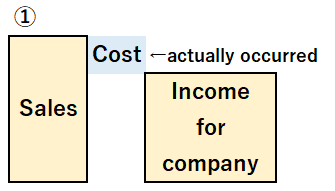

①売上高ー経費=法人の利益(個人事業主でいう所得)

まず、上の式で法人は消耗品費や交際費といった必要経費を利用することができています。上記に法人の利益とありますが、これと役員給与を同額として支給したと仮定します。役員給与は消耗品や交際費と同様に法人の損金となりますから、法人の利益はゼロとなり、法人にかかる税金は最低限の金額で済むことになります。

②売上高ー(経費+役員給与)=利益0円→法人に係る税金は最低水準(通常は住民税均等割額の7万円)

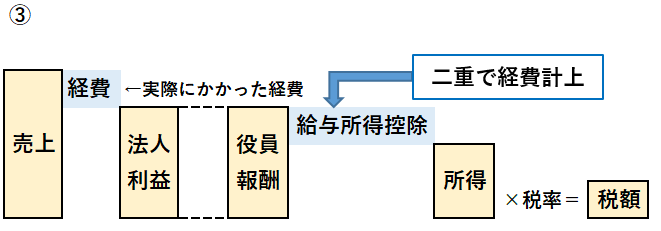

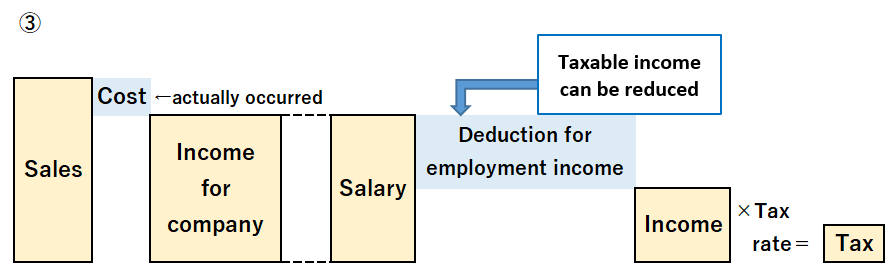

そして、もらった役員報酬はどうでしょう。

③役員給与-給与所得控除=法人成りした場合の個人所得

このように、法人成りした場合は給与所得控除を利用することができます。

法人成りをすることで、法人の事業で必要な経費を法人の損金(必要経費)として使える上に、給与所得控除も使えるわけです。

一方、個人事業主の場合には、給与所得控除が使えません。このため、①の式にあるように、必要経費のみを控除した段階が個人の所得となって、そこから所得税の税金が計算されます。

このように、必要経費と給与所得控除の二重取りをすることができ、税金を節約することが可能になるのです。

ここで、①個人事業主として所得税を計算した場合と、②法人を設立して所得税を計算した場合の2通りについて、具体的な数値で比べてみましょう。

【計算の前提】

・売上:1,000万円

・経費: 200万円

①個人事業主として所得税を計算した場合

個人所得:800万円(売上1,000万円ー経費200万円)

個人税額:800万円×23%ー636,000円=1,204,000円

②法人を設立して所得税を計算した場合

法人所得:0円(売上1,000万円ー経費200万円ー役員報酬800万円)

法人税額:法人住民税均等割額の7万円のみ

個人所得:600万円(給与800万円ー※給与所得控除200万円)

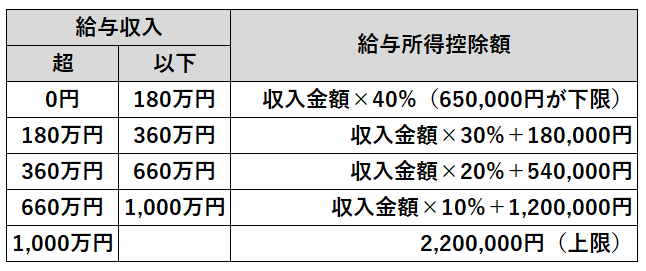

※給与所得控除:給与800万円×10%+1,200,000円=200万円

個人税額:600万円×20%ー427,500円=772,500円

合計税額:70,000円+772,500円=842,500円

このように法人を設立して役員報酬という形で受け取ることにすれば、給与所得控除のしくみを利用して税金の額を減らすことができます。上の例では実に361,500円もの節税となりました。個人事業主の方は、ぜひ検討してみてください。弊事務所にて簡単にシミュレーションすることもできますので、お気軽にお問い合わせください。

こんな悩みごとはありませんか?

- 担当者が毎年のように変わる

- 税理士が高圧的で意見交換できない

- 税理士から節税策など何の提案もない

- 試算表をタイムリーに出してくれない

- 試算表の説明を受けたことがない

- クラウド会計に対応していない

- ほとんど税理士が来てくれない

- 質問しても回答がない、嫌な顔をされる

- 現在の税理士が高齢でこの先が不安

税理士とのコミュニケーション不足は、記帳内容がぐちゃぐちゃになり、誤った経理処理となる要因となります。

その結果、3~5年周期の税務調査において指摘の対象となり、最大40%の追徴課税(追加で税金が取られてしまうこと)のリスクが高まります。

無駄な税金を払わないためには、常日頃、経理処理や経営環境などについて税理士と共有し、追徴課税リスクへの対応策を早期に講じることが大切です。

岩沢将志税理士事務所では、『日本一気軽に相談できる税理士』を理念に掲げた代表税理士が、経理内容のご相談はもちろん、税務調査対策(税務調査にて指摘が予想される事項を早期にお伝え)、お客様に最適な節税策のご提案等をさせていただいております。

ただいま、初回限定の無料コンサルティングを実施しております。

強引な勧誘は一切しておりませんので、お気軽にお問合せいただければと思います。

~常に代表税理士が責任をもって対応いたします~

You have several options to reduce your tax if you set up a company. One of them is the scheme where you can deduct both the cost which actually occurred and the one calculated using a fixed formula regardless of how much you actually spend (給与所得控除:Deduction for employment income). In this scheme, you record your actual cost for a company while you subtract the amount of deduction for employment income from your salary. This led to less taxable income which means less amount of tax.

How to calculate income tax for those who are self employed?

To make it simple, first you calculate your taxable income by subtracting the amount of cost from the amount of sales. Next you calculate your tax amount.

【Taxable income (Sales – Cost) ×Tax rate】

Please be noted that the progressive tax rate is applied in Japan. It means the more you earn, the higher the tax rate becomes. 45% tax rate is applied for those who earn more than 40 million JPY taxable income.

【What is Deduction for employment income?】

One of the most important thing to reduce your tax when you set up a company is the deduction for employment income. The amount of deduction for employment income is calculated using a fixed formula according to your salaries and wages. Therefore, actual expenses incurred are not subtracted when calculating employment income.

As mentioned above, Those who are self employed subtract the cost which actually occurred from the taxable income while directors and employees subtract the cost which is calculated by a certain formula based on their salaries and wages. You might want to use both of them. Yes, you can. Of course legally when you set up a company.

To make it simple, let’s say the exact same amount of income for the company will go to director’s remuneration.

【①Sales – Cost = Income for the company】

The company subtract the expenses such as office supplies and entertainment expenses. Director’s remunerations are also recognized as company expenses which leads to no taxable income for the company. Therefore, the company pays a minimum amount of taxes.

【②Sales – (Cost + Director’s remunerations) =No taxable income for the company → minimum tax for the company】

Then, how about the amount of individual tax for the director’s remunerations?

【③Director’s remunerations – Deduction for employment income = Individual income】

As shown in above table, you can record expenses which isn’t actually spent in addition to actual expenses if you set up a company. You can never use this scheme as long as you work as a sole proprietorship.

As above mentioned, there is a merit when you set up a company. Let me give you an example. Following is a comparison how much tax you owe between a situation where you are a sole proprietorship and a situation where you set up a company.

【We will hypothesize that…】

・Amount of sales:10,000,000 JPY

・Amount of costs: 2,000,000 JPY

①How much tax you owe if you are a sole proprietorship?

Income:8,000,000 JPY (10,000,000 JPY – 2,000,000 JPY)

Tax:8,000,000 JPY×23% – 636,000 JPY = 1,204,000 JPY

①How much tax you owe if you are set up a company?

Income for company:0 JPY (10,000,000 JPY – 2,000,000 JPY – 8,000,000 JPY Salary)

Tax for company:Minimum (basically 70,000 JPY)

Income for individual:6,000,000 JPY (8,000,000 JPY Salary – ※2,000,000 JPY Deduction for employment income)

※Deduction for employment income:8,000,000 JPY Salary×10% + 1,200,000 JPY = 2,000,000 JPY

Tax for individual:6,000,000 JPY×20% – 427,500 JPY = 772,500 JPY

Total tax:70,000 JPY+772,500 JPY=842,500 JPY

⇒(361,500 JPY tax saving)

With this scheme, you can alleviate your tax burden. This is a chance for those who are self employed. Get in touch and get an estimate!